by Team Tradify, February 20, 2024

When you start a trade business there are several legal and financial obligations to wrap your head around. Things like paying your tax bill and complying with HMRC’s VAT rules. When you decide to hire your first staff member, you’ll find there are even more responsibilities.

Thinking of hiring an apprentice? Download our free Interview Questions for Apprentices.

In the UK, self-employed tradespeople also need to consider the Construction Industry Scheme (CIS) if they work in the construction industry.

It’s unlikely, that as a sole trader, you chose to start your own trade business to spend all your time fretting about your finances. To help you keep on top of your legal responsibilities and all the pesky financial fine print, here’s what you need to know about CIS.

Skip ahead:

- 1. What is CIS?

- 2. How CIS affects you

- 3. CIS for contractors and subcontractors

- 4. Work covered by CIS

- 5. CIS in action

- 6. Registering for CIS

- 7. VAT reverse charge

- 8. Spend less time managing CIS tax requirements

- 9. CIS with Tradify & Sage

- 10. VAT reverse charge with Tradify & Sage

- 11. CIS with Tradify & Xero

1. What is the Construction Industry Scheme?

CIS isn’t a new piece of legislation – it was introduced in 1971 to combat serious tax evasion in the industry. Several changes have been made over the years, with the UK government announcing the most recent developments at the end of 2020. These latest changes come into effect on 1 March 2021.

The scheme sets out the rules for how payments to subcontractors for construction work must be handled by contractors in the construction industry and certain other businesses. It’s similar to PAYE for employees – but for subcontractors.

Under the scheme, all payments made from contractors to subcontractors must factor in the subcontractor’s tax status as determined by the HMRC. This means contractors may be required to deduct a portion of the money due to the subcontractors (minus the cost of materials) – which they then pay to HMRC.

That money counts as advance payment towards the subcontractor’s tax and National Insurance.

2. How the Construction Industry Scheme affects you

So, why do you need to understand CIS – and what are the implications for trade business owners? If you’re self-employed in the building or construction trade, then it’s likely you’ll need to pay tax under CIS.

Failing to register as a contractor could lead to penalties in the tens of thousands of pounds (irrespective of whether workers are registered as self-employed and have paid their tax bill). Contractors must register for the scheme.

Subcontractors don’t have to register, but deductions are taken from their payments at a higher rate (30%) if they’re not registered (versus 20% if they are). That’s a lot of extra cash to fork out when you could be using it to grow your trade business in other ways.

3. The difference between contractor and subcontractor

Under CIS, a contractor is someone who:

- Pays subcontractors for construction work, or

- Owns a business that doesn’t do construction work, but spends more than £1 million a year on construction in any three-year period.

Under CIS, a subcontractor is:

- Paid to do construction work by a contractor

If you fall under both categories, you must register as both a contractor and a subcontractor.

4. Work covered by CIS

Another factor is the type of construction work. CIS covers:

- Construction of a permanent or temporary building or structure

- Civil engineering work like roads and bridges

- Site preparation (e.g. laying foundations and providing access works)

- Demolition and dismantling

- Building work

- Alterations, repairs and decorating

- Installing systems for heating, lighting, power, water and ventilation

- Cleaning the inside of buildings after construction work

However, there are some exceptions:

- Architecture and surveying

- Scaffolding hire (with no labour)

- Carpet-fitting

- Manufacture of materials used in construction (including plant and machinery)

- Delivering materials

- Work on construction sites that’s clearly not construction, e.g. running a canteen or site facilities

5. An example of CIS in action

You’re asked by a friend named Dave to do some repair work on his private home. To complete the job, you ask another self-employed tradesperson named Jared to help you.

Dave pays you without the deduction of CIS tax because he is a private homeowner. You then pay Jared for his work on the job.

In this example, you would need to register under CIS as a contractor before you pay Jared. You’ll also need his UTR number and check his CIS status with HMRC.

When you pay Jared, you will need to deduct a percentage depending on his status with HMRC. If HMRC advises that Jared is registered under CIS (but not for gross payment), then you’ll keep back the required 20% of tax and pay this to HMRC on Jared’s behalf.

If you fail to register as a contractor under CIS, you could face penalties for not keeping CIS records, and a monthly penalty per missed CIS return (which are due monthly).

6. Getting registered for CIS

When you start your own trade business as a sole trader, you need to register as self-employed for Self-Assessment. You also need to register under CIS. Yes, there are two separate registrations but both can be done at the same time.

Registering as a CIS contractor

-

You must register for CIS before you take on your first subcontractor.

-

Find out if you should employ the person instead of subcontracting the work. You may get a penalty if they should be an employee instead.

-

Check with HMRC that your subcontractor is registered with CIS.

-

When you pay subcontractors, you’ll usually need to make deductions from their payments and pay the money to HMRC.

-

You’ll need to file monthly returns and keep full CIS records – you may get a penalty if you do not.

Registering as a CIS subcontractor

You should register for CIS if you work for a contractor and you’re one of the following:

- Self-employed

- The owner of a limited company

- A partner in a partnership or trust

Under CIS, a contractor must deduct 20% from your payments and pass it to HMRC. These deductions count as advance payments towards your tax and National Insurance bill. If you do not register for the scheme, contractors must deduct 30% from your payments instead.

When you register for CIS, you can apply for gross payment status if you do not want deductions to be made in advance by contractors. For this, you’ll need to meet specific criteria. You do not need to register for CIS if you’re an employee.

7. VAT reverse charge

From 1 March 2021, the way Value-Added Tax (VAT) works has changed. VAT no longer gets passed between VAT registered businesses in the construction industry. Suppliers are no longer required to charge or receive VAT from their contractors.

Instead, main contractors essentially charge themselves VAT for subcontractors’ services, and pay the money that would have been paid to the subcontractor, direct to HMRC in their VAT returns. The new rules also apply to goods, where those materials are provided alongside services specified in the CIS.

- Learn more about when to use VAT reverse charges.

- See how VAT reverse charges work with Tradify & Sage.

8. Spend less time managing your CIS tax requirements

As a trade business owner/operator, one minute you’re knee-deep in mud or electrical wires, the next you’re busy quoting for new work, sending out invoices, and chasing payments.

Paying CIS tax can add more complexity to your admin but technology can help you cut down the time you spend managing subcontractor tax. Even better, integrated systems like construction project management software can boost the speed of your workflow – increasing your overall productivity while ensuring you stay ahead of your tax obligations.

When integrated with Sage or Xero, Tradify works seamlessly to help you out when it comes to subcontractor invoices and bills that fall under the CIS scheme. When you submit your monthly CIS returns through your accounting software, you’ll have all the necessary information you need to speed up the verification process, deduct the correct tax rates and submit your payments on time.

Thanks to technology, less time worrying about your tax requirements means more time on the tools, driving growth in your business, or just relaxing.

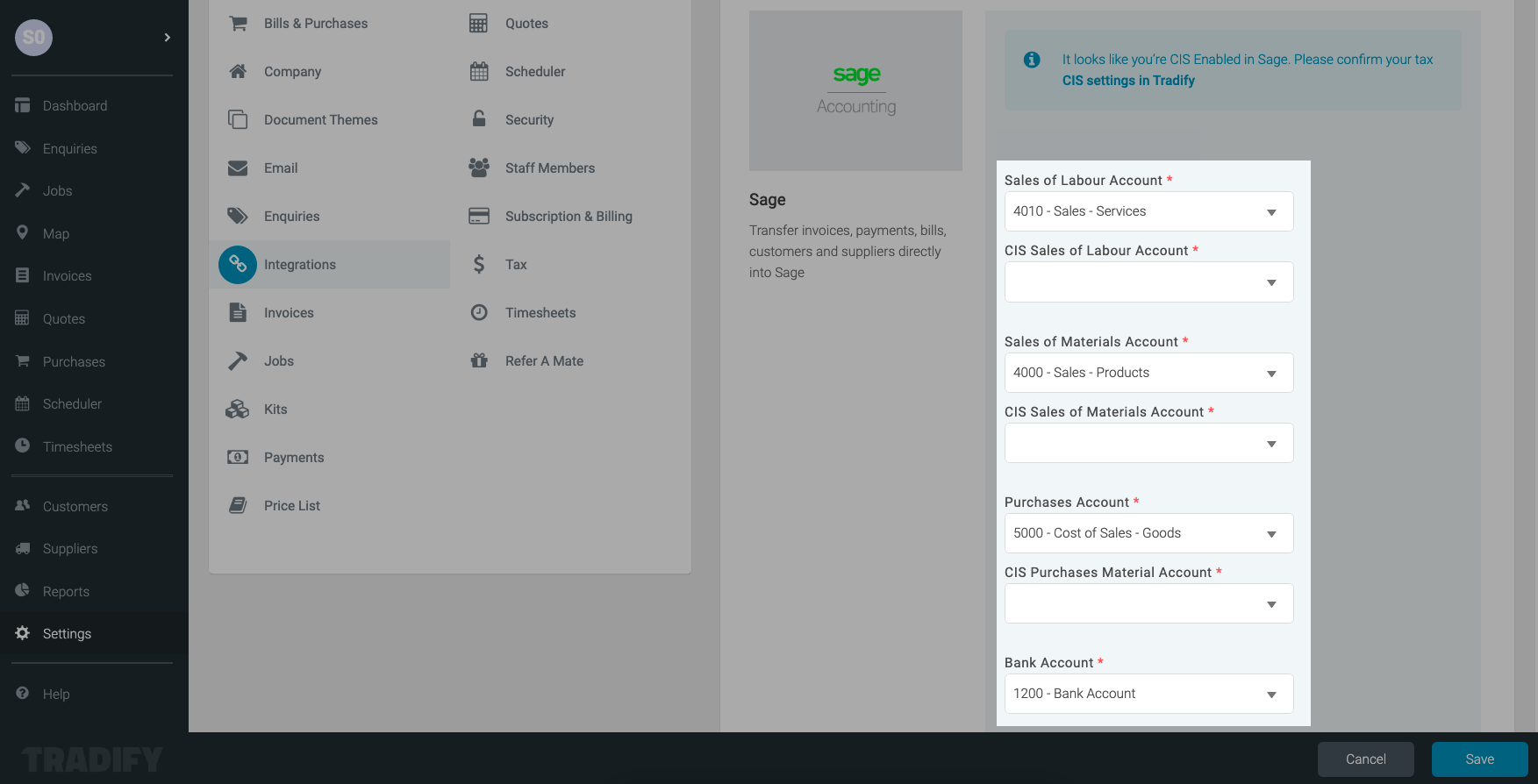

9. CIS with Tradify & Sage

To use the CIS function with Tradify and Sage, first you'll need to enable CIS in your Sage account.

Connecting Sage to Tradify will help you manage number of CIS requirements, including:

- Mapping CIS Account Codes

- Viewing your CIS VAT Settings

- Creating Invoices with CIS

- Creating Bills with CIS

Learn more about complying with CIS requirements using Tradify & Sage.

10. VAT reverse charges with Tradify & Sage

To utilise the Reverse VAT function with your Tradify-Sage integration, you'll first need to enable Reverse VAT in your Sage account. To achieve this (and to learn more about Reverse VAT), read this article.

Enabling Reverse VAT for a customer

When creating a new invoice, Tradify will first check to see if the customer has Reverse VAT enabled in Sage. If they do, the customer record in Tradify will be updated to match (as show below).

To learn about invoicing customers with reverse VAT, check out our Reverse VAT & Sage help article.

11. CIS with Tradify & Xero

To use the CIS function with Tradify and Xero, first you'll need to enable CIS in your Xero account.

Connecting Xero to Tradify will help you manage number of CIS requirements, including:

- Mapping CIS Account Codes

- Viewing your CIS VAT Settings

- Creating Invoices with CIS

- Creating Bills with CIS

Learn more about complying with CIS requirements using Tradify & Xero.

Take Tradify for a free 14-day test-drive or pop into one of our live demo webinars to see the app in action.

Work out your hourly rate with our free Charge-Out Rate Calculator!

WightStream Cleans Up Their Scheduling With Tradify

How to Be a Great Boss

What is a Quality Control Checklist?

Give Tradify a go for free!

Save 10+ hours/week on business admin with the highest-rated job management software for tradespeople.

With free one-on-one training and phone support, it's never been easier to get started.